AP Microeconomics Market Structure Review

Assessment

•

Bryan Burns

•

Social Studies

•

11th Grade - University

•

48 plays

•

Medium

Improve your activity

Higher order questions

Match

•

Reorder

•

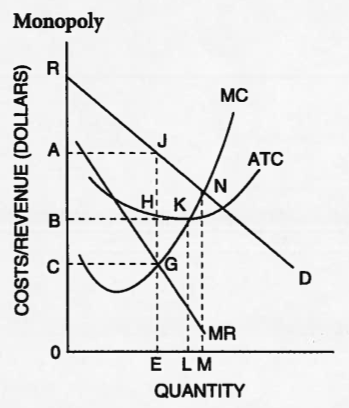

Categorization

.svg)

actions

Add similar questions

Add answer explanations

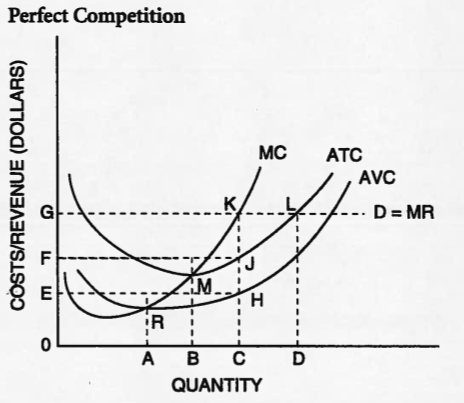

Translate quiz

Tag questions with standards

More options

58 questions

Show answers

1.

Multiple Choice

oligopsony

monopoly

monopsony

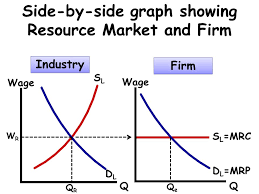

perfectly competitive factor market and firm

2.

Multiple Choice

What does marginal mean in the language of economics?

Additional

Less

Satisfaction

I can't believe it's not Butter.

3.

Multiple Choice

What does utility mean in the language of economics?

Additional

Less

Satisfaction

I can't believe it's not Butter.

4.

Multiple Choice

If every consumers needs are being met perfectly and every good that is being made is being sold, what type of efficiency is being achieved?

Productive Efficiency

Allocative Efficiency

5.

Multiple Choice

When there is only one seller of a good or service, they are said to have a?

Monopoly

Oligarchy

Monopolistic Competition

Perfect Competition

6.

Multiple Choice

When there are only a few sellers of a type of produce, like Smart phones, there is said to be an?

Monopoly

Oligopoly

Monopolistic Competition

Perfect Competition

7.

Multiple Choice

When there is lots of competition in a market because the barriers to entry are low and there are many substitutes that exist, this is called?

Monopoly

Oligopoly

Monopolistic Competition

Perfect Competition

8.

Multiple Choice

monopoly

oligipoly

perfect competition

monopolistic competition

9.

Multiple Choice

perfect competition

monopolistic competition

monopoly

oligopoly

10.

Multiple Choice

Which of the following is true about an imperfectly competitive firm’s marginal revenue (MR) curve if it has a linear and downward-sloping demand curve?

MR decreases at an increasing rate.

MR increases at first, then decreases.

MR is constant.

MR decreases and is less than demand.

MR is greater than demand.

11.

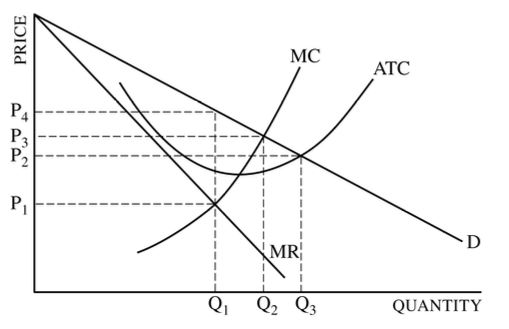

Multiple Choice

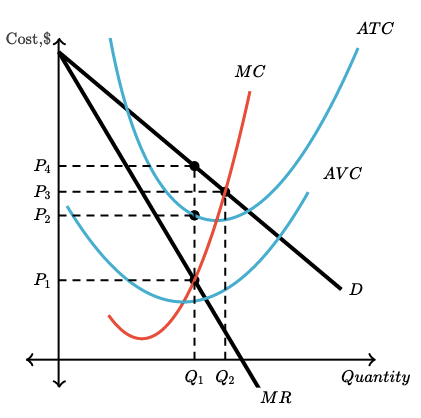

For the graph shown here, what quantity will this firm produce and what price will it charge?

Q2 ; P2

Q2 ; P3

Q1 ; P1

Q1 ; P2

Q1 ; P4

12.

Multiple Choice

P=Increase; Q=Increase

P=Increase; Q=Decrease

P=Decrease; Q=Decrease

P=No Change; Q=Increase

13.

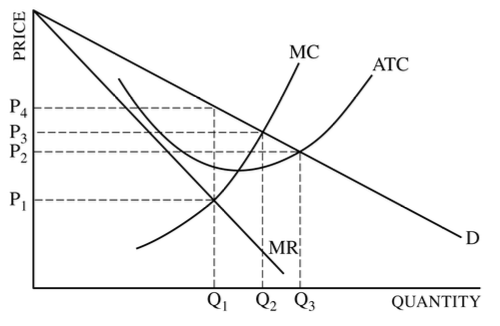

Multiple Choice

Q1 & P1

Q2 & P3

Q1 & P4

Q3 & P2

14.

Multiple Choice

Q1 & P1

Q2 & P3

Q1 & P2

Q3 & P2

15.

Multiple Choice

earn a higher profit

increase consumer surplus

decrease deadweight loss

make its demand more elastic

16.

Multiple Choice

P=Higher; Q=Same

P=Lower; Q=Same

P=Lower; Q=Higher

P=Higher; Q=Lower

17.

Multiple Choice

Q1, price at P3, and earn an economic profit

Q1, price at P1, and suffer a loss

Q2, price at P2, and earn an economic profit

Q2, price at P2, and earn only a normal profit

18.

Multiple Choice

A

B

C

R

19.

Multiple Choice

0CGE

0AJE

AJHB

BAJN

20.

Multiple Choice

BKL0

CGE0

AJE0

BHE0

21.

Multiple Choice

0CGE

0AJE

AJHB

BAJH

22.

Multiple Choice

ABHJ

AJGC

ARJ

ARJE

23.

Multiple Choice

A

B

C

D

24.

Multiple Choice

K

M

L

R

25.

Multiple Choice

0GKC

FGKJ

0EHC

0FJC

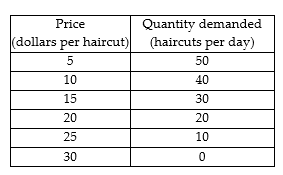

26.

Multiple Choice

Christy's Haircuts, the sole supplier of haircuts in a small town, faces the demand schedule shown in the table above. What is Christy's marginal revenue from the 25th haircut?

zero

$5

$7

$5.50

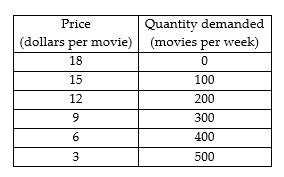

27.

Multiple Choice

Roxie's Movie Theatre is the only one in town. The table above gives the demand schedule for movies. If Roxie's is a single-price monopoly and the marginal cost of a movie is $6, Roxie's will charge ________ a movie and will sell ________ movie tickets a week.

$15; 100

$12; 200

$6; 400

$9; 300

28.

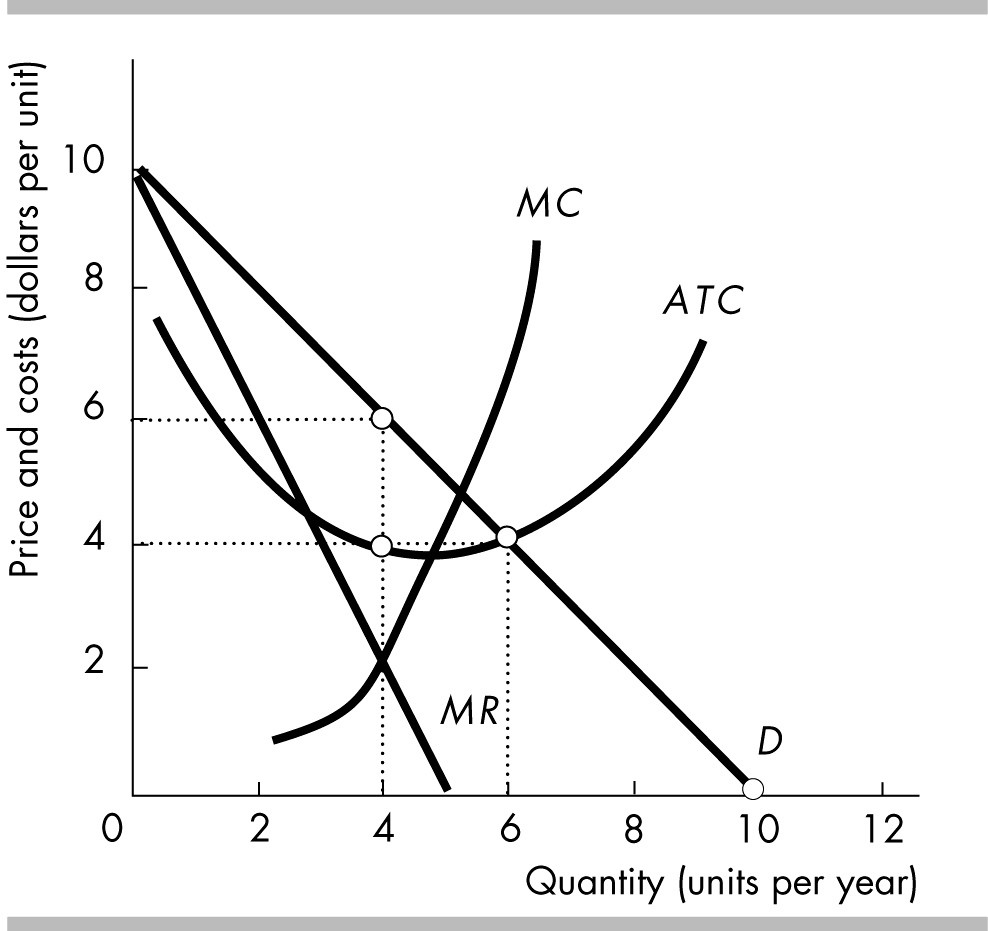

Multiple Choice

For the unregulated, single-price monopoly shown in the figure above, when its profit is maximized, output will be

4 units per year and the price will be $6.

4 units per year and the price will be $4.

6 units per year and the price will be $4.

None of the above answers is correct.

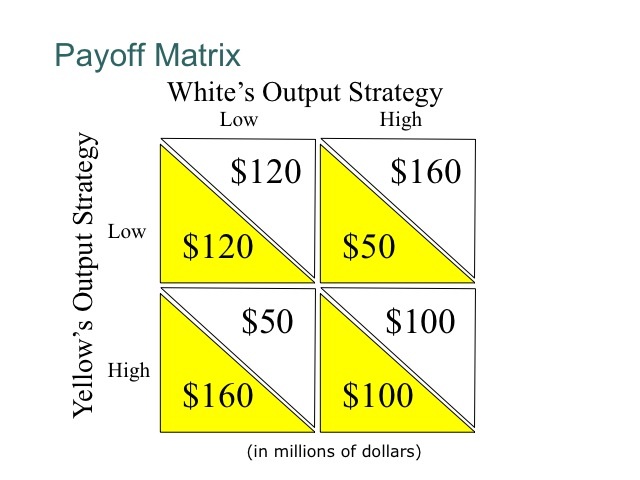

29.

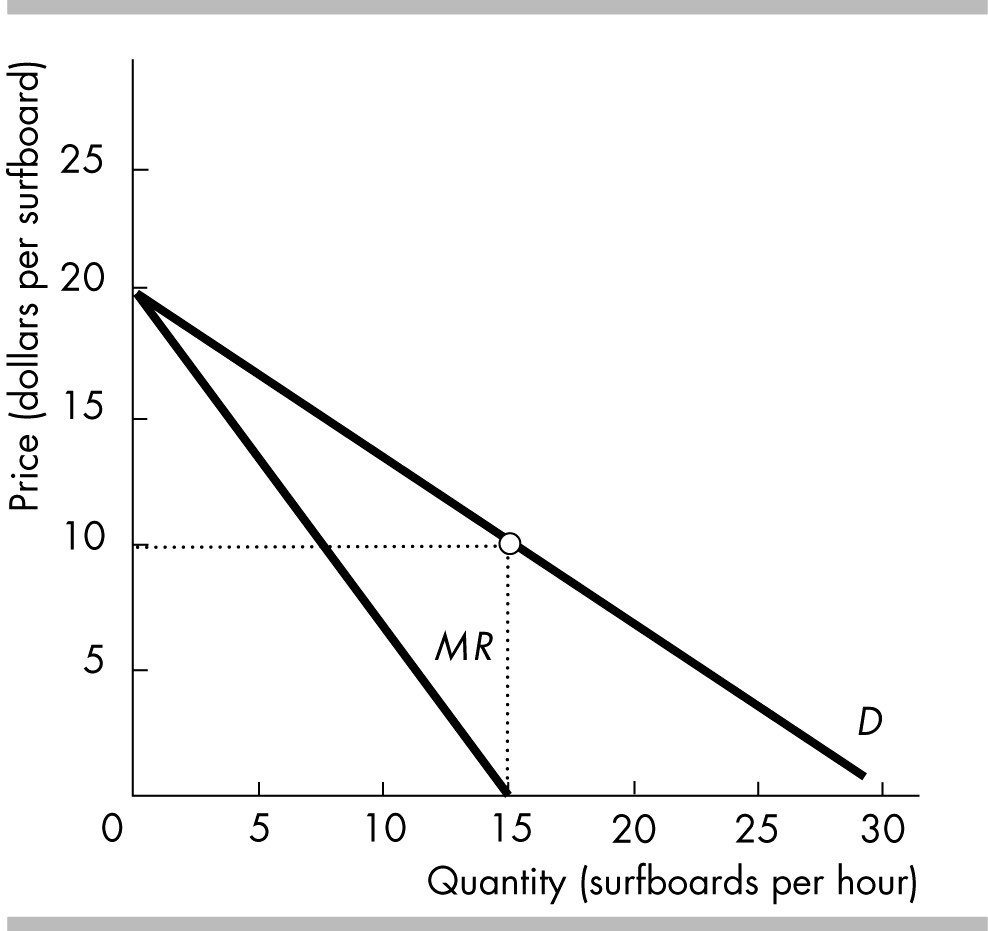

Multiple Choice

Sue's Surfboards is the sole renter of surfboards on Big Wave Island. Sues demand and marginal revenue curves are illustrated in the figure above. Sue's Surfboards currently rents 15 surfboards an hour. Sue's total revenue from the 15 surfboards is

$300

$220

$150

$100

30.

Multiple Choice

In long-run equilibrium, the marginal benefit exceeds the price charged by the firms.

In long-run equilibrium, the price is greater than the marginal cost.

In long-run equilibrium, average total costs are minimized.

In long-run equilibrium, the firm is earning economic profits.

31.

Multiple Choice

Monopoly

Monopolistic Competition

Perfect Competition

Oligopoly

32.

Multiple Choice

Price equals marginal cost and average total cost.

Price equals average total cost but is greater than marginal cost.

Price equals marginal cost and is greater than average total cost.

The firm earns positive economic profits by producing at minimum average cost.

33.

Multiple Choice

making a profit in the short-run

incurring a loss in the short-run

making a profit in the long-run

breaking even in the long-run

34.

Multiple Choice

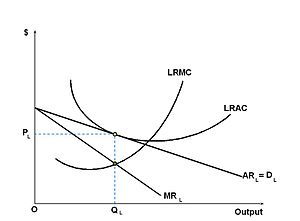

MC = marginal cost, and ATC = average total cost. In monopolistic competition, which of the following most accurately describes the long-run equilibrium conditions for a firm?

P>ATC, MR=MC, and P>MC

P=ATC, MR=MC, and P=MC

P=ATC, MR=MC, and P>MC

P=ATC, MR>MC, and P>MC

35.

Multiple Choice

shift the demand curve for its product to the left

make its product more similar to its competitors’

reduce the industry’ s barriers to entry

make the demand for its product less price elastic

36.

Multiple Choice

Perfect Competition

Monopolistic Competition

Oligopoly

37.

Multiple Choice

Define collusion

When two cars collide on the road

a secret agreement between two competing firms to sell their similar products at the same price

38.

Multiple Choice

monopoly

oligopoly

perfect competition

monopolistic competition

39.

Multiple Choice

maintain existing prices.

raise their prices.

go out of business.

lower their prices.

40.

Multiple Choice

Game theory is used to explain

why firms price discriminate

how monopolies evolve into oligopolies

strategic behavior of firms in oligopoly

profit maximization in monopoly

price leadership of monopolistic competition

41.

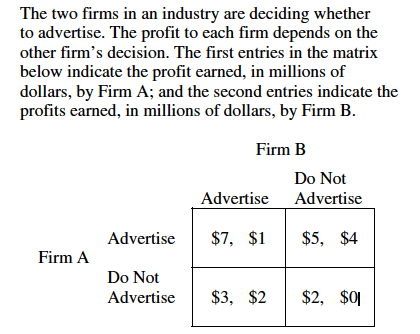

Multiple Choice

Based on the payoff matrix, which of the following is correct?

Firm A always gets a smaller share of the industry profits.

Firm A’s dominant strategy is to advertise.

Firm B’s dominant strategy is not to advertise.

The dominant strategy for both firms is not to advertise.

Neither firm has a dominant strategy.

42.

Multiple Choice

In the long run, new firms will enter a monopolistically competitive industry:

provided economies of scale are being realized.

even though losses are incurred in the short run.

until minimum average total cost is achieved.

until economic profits are zero.

43.

Multiple Choice

A monopolistically competitive firm maximizes profits or minimizes losses in the short run by

Setting price equal to marginal cost.

Producing at the output level where ATC is minimized.

Producing at the output level where MR equals MC.

Producing at the output level where MC equals ATC.

44.

Multiple Choice

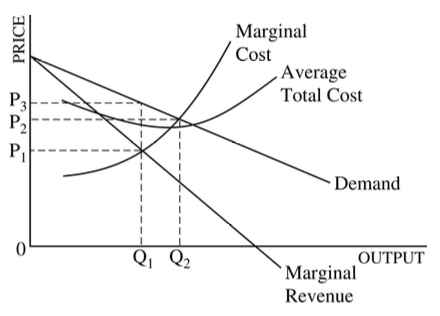

In the above figure, the monopolistically competitive will experience what change into the long run?

a right shift of it's demand curve.

a left shift of it's demand curve.

a right shift of it's supply curve.

a left shift of it's supply curve.

45.

Multiple Choice

If this graph is for a monopolistically competitive firm, it best represents

short run economic loss.

short run extra-normal profit.

long run economic profit.

long run equilibrium at normal profit.

short run accounting loss.

46.

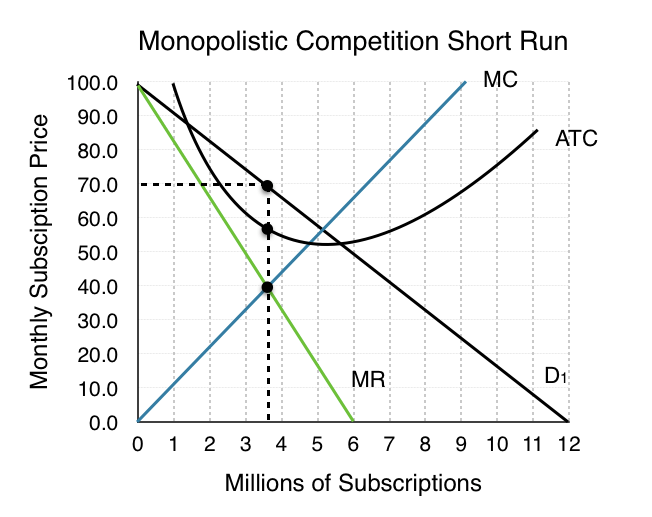

Multiple Choice

This firm will charge a price of _____ and make a per unit ___ of _____.

70; loss; 10.

60; normal profit; 0.

70; profit; 3.5.

60: profit; 10.

70; profit; 10.

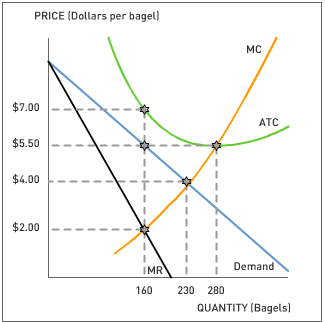

47.

Multiple Choice

This firm will charge a price of _____ and make a per unit ___ of _____.

7; loss; 1.5.

7; normal profit; 0.

7; profit; 1.5.

5.5: loss; 1.5.

5.5; profit; 1.5.

48.

Multiple Choice

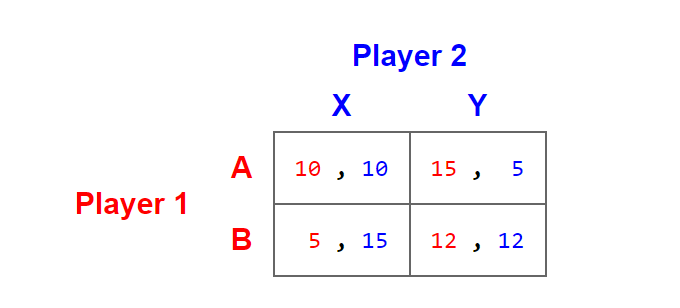

A,X

A,Y

B,X

B,Y

49.

Multiple Choice

The cartel model of oligopoly predicts that

all firms in the industry act in unison to set monopoly price

each producer acts independently of others

firms follow the low-price firm in the industry

differences in cost of production discourage individual firms from cheating

the markup on marginal cost should be the same for all firms

50.

Multiple Choice

high

low

51.

Multiple Choice

What would facilitate collusion between firms in an oligopolistic industry

An increase in the number of firms

large fluctuations in demand

rapid changes in technology

a standardised product

52.

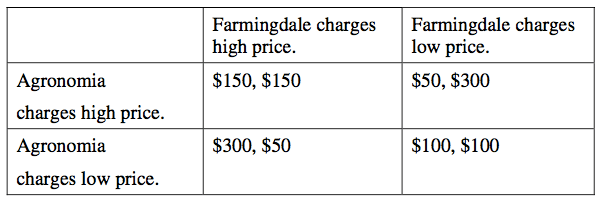

Multiple Choice

Agronomia = $50; Farmingdale = $100

Agronomia = $150; Farmingdale = $150

Agronomia = $300; Farmindale = $50

Agronomia = $100; Farmingdale = $100

53.

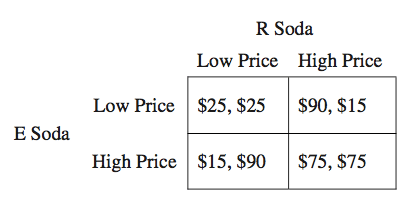

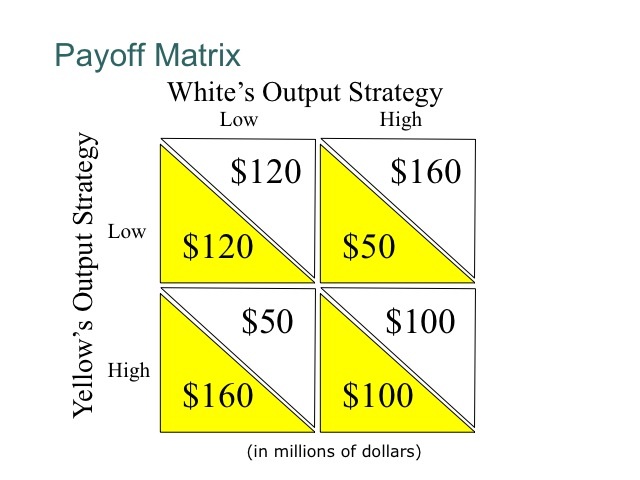

Multiple Choice

the soft-drink industry. The companies cannot cooperate. Each firm can follow a high-price strategy or a low-price strategy for pricing its product. In the payoff, the first entry in each cell shows the profits to E Soda and the second entry shows the profits to R Soda. It can be concluded that:

neither E Soda nor R Soda has a dominant strategy

E Soda has a dominant strategy but R Soda does not

Both firms will choose the high-price strategy

Both firms will choose the low-price strategy

54.

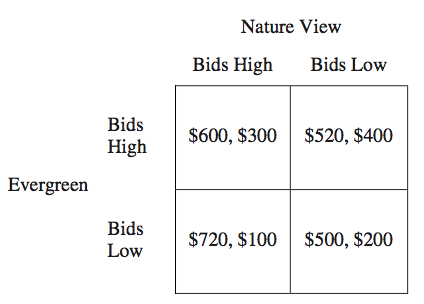

Multiple Choice

a landscaping contract. The payoff matrix shows what each firm’s total weekly profits from all its operations will be for each combination of bids. The first entry in each cell shows Evergreen’s profit, and the second entry in each cell shows Nature View’s profit. A Nash equilibrium results under which of the following conditions?

When both firms bid low

When Evergreen bids high and Nature View bids low

When both firms bid high and when both firms bid low

When Evergreen bids low, no matter what Nature View’s bid is

55.

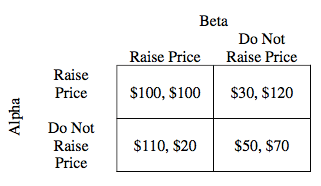

Multiple Choice

Alpha: Do Not Raise; Beta: Do Not Raise

Alpha: Do Not Raise; Beta: Raise

Alpha: No Dominant Strategy; Beta: Raise

Alpha: Raise; Beta: Do Not Raise

56.

Multiple Choice

A,X

A,Y

B,X

B,Y

57.

Multiple Choice

high

low

58.

Multiple Choice

Oligopoly, Monopoly, Perfect Competition, Monopolistic Competition

Perfect Competition, Oligopoly, Monopoly, Monopolistic Competition

Monopoly, Oligopoly, Monopolistic Competition, Perfect Competition

Monopoly, Monopolistic Competition, Perfect Competition, Oligopoly

Explore this activity with a free account

Find a similar activity

Create activity tailored to your needs using

Market Structures

•

9th - 12th Grade

Supply and Demand

•

5th Grade

Economy

•

4th Grade

Demand

•

12th Grade

Demand & Law of Demand

•

9th - 12th Grade

Supply and Demand

•

2nd Grade

Macroeconomics

•

12th Grade

Monetary and Fiscal Policy

•

9th - 12th Grade